What are the rules if you inherit someone’s IRA?

Inheriting investments from a loved one is typically pretty straightforward. When the estate settles, assets transfer into your name. Inheriting investments from an Individual Retirement Account (IRA) is a little more complicated. There are rules about making withdrawals. If you don’t pay attention to them, there can be tax consequences.[i]

Many People Have few Options

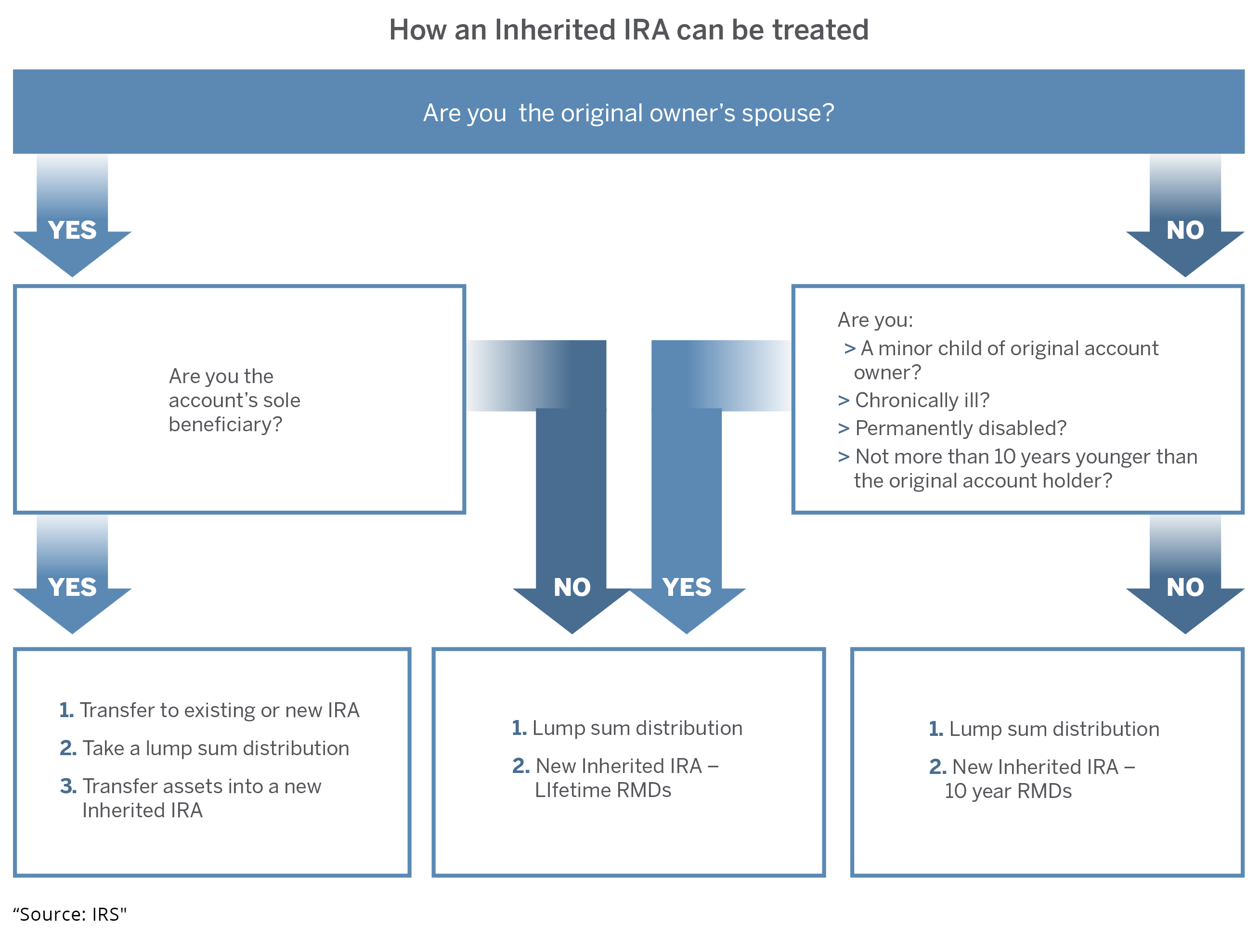

Generally speaking, people who inherit an IRA have two options.

- Take a lump sum distribution

- Transfer assets into a new Inherited IRA

A lump sum distribution is taxable income. If it’s big enough, it may put you in a higher tax bracket. But it won’t trigger the early withdrawal penalty imposed on people younger than 59½ years old.[ii]

Transferring assets into an Inherited IRA can help prevent the spike in income caused by a lump sum distribution…as well as the tax bill that comes with it.[iii] And you’ll have to start making withdrawals no later than the end of the next calendar year.

These withdrawals are Required Minimum Distributions (RMDs). You don’t have a choice. They must be taken. If not, there is a 50 percent tax levied on any shortfall not withdrawn by the end of the year that they’re due. After that, all the money in the account must be withdrawn within 10 years of the inheritance.

The rules are subtly different for eligible designated beneficiaries.

Who are Eligible Designated Beneficiaries?

The surviving spouse of the original IRA account owner is considered an eligible designated beneficiary. So are the original account owner’s minor children. Any named beneficiaries who are chronically ill or permanently disabled are also eligible designated beneficiaries. So are beneficiaries who are not more than 10 years younger than the original account holder (e.g., brothers or sisters).

Eligible designated beneficiaries have several options when they inherit a loved one’s IRA.

Non-spouse Beneficiaries

Eligible designated beneficiaries can opt to receive lump sum distributions from the IRAs they inherit or they can transferring assets directly to an Inherited IRA.

An Inherited IRA requires them to take annual RMDs. But the duration of those withdrawals depends on when the original IRA account owner passed away.

- If the original owner passes away before the date that his or her own RMDs were scheduled to begin, then the beneficiary’s RMDs would be based on the beneficiary’s life expectancy.[iv]

- If the original owner passes away after the date RMDs were schedule to begin, then the beneficiary would use the longer of his or her own life expectancy or that of the original account owner.[v]

These same rules apply to a surviving spouse who is not the sole beneficiary of a late spouse’s IRA.

When a Spouse is the Sole Beneficiary

A surviving spouse who is the sole beneficiary of a late spouse’s IRA can take a lump sum distribution or open an Inherited IRA and begin taking RMDs. But there is another option. He or she can transfer the late spouse’s IRA into a new or existing Traditional IRA.

Transferring the IRA into your own allows it to be treated as if you were the original owner. The transfer is not taxable and this treatment allows you to:

- Contribute to the account

- Consolidate it with your other IRAs

- Roll over a former employer’s retirement plan into it

It also means that the account can grow tax free and that you can name your own beneficiaries. You can also withdraw funds whenever you like (subject to income taxes and potential early withdrawal penalties).

Seek Professional Advice

If you’ve inherited someone’s IRA, seeking the advice of qualified tax and estate planning professionals can help. It also makes sense to work with an investment professional who can help you understand how inherited investments might fit into your financial plan. We’re here to help at (800) 235-8396.

i This article assumes the original IRA account holder died after 2019 and that rules created by the SECURE Act apply. The source of information used here is the Department of the Treasury, Internal Revenue Service, Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs) For use in preparing 2021 Returns.

Investors should consult with qualified tax and estate planning professionals for guidance.

ii Most distributions from an IRA become taxable income in the year they are withdrawn and those taken before the account holder reaches age 59½ are typically subject to an additional 10 percent early withdrawal penalty.

iii You must open a new Inherited IRA even if you have an existing one. Inherited IRAs cannot be combined unless they are trustee-to-trustee transfers from the same deceased IRA owner with you as beneficiary.

iv The IRS maintains life expectancy tables to help calculate RMDs.

v Beneficiaries who are minor children using their life expectancy to determine initial RMDs must convert to the 10-year rule and deplete Inherited IRAs within 10 years after reaching the age of majority.