Retirement planning is a straightforward process intended to help you maintain a specific lifestyle after you stop working. Retirement planning means setting long-term goals and employing assets to achieve them. The process relies on a few practical steps: using tax-advantaged savings vehicles like your employer’s retirement plan and/or an IRA and managing investment risk, expenses and debt.

A Streamlined View of Retirement Planning

The broad retirement planning process may be aided by employing three straightforward techniques.

- Start early and take advantage of employer plans

- Limit credit card use

- Manage Social Security

Start Early and Take Advantage of Employer Plans

Time is the most powerful variable in the retirement planning equation. The more time you have to save, the more you can accumulate.

The longer you wait, the greater the potential missed opportunity. Waiting to save could impact your future wealth.

Starting as early as possible is an important technique in retirement planning. The amount you start with is less critical than actually starting – even if the initial amount is small. Future contributions can increase at a pace commensurate with career advancement and pay increases.

Another powerful variable is your employer’s retirement plan (e.g., 401(k), 403(b), 457, TSP). Here too, the initial amount saved isn’t as important as the commitment to do it.

Making contributions to an employer’s retirement plan is relatively easy since they are typically made by payroll deduction. Many financial professionals recommend contributing between 10 percent and 25 percent of your annual salary based on your age.

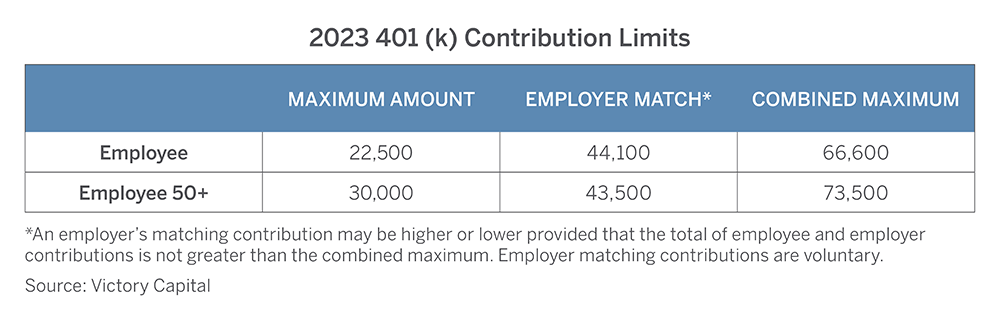

Younger workers can be at the lower end of these percentages because they have the benefit of time on their side. Older workers might need to save more. As the table below shows, those age 50 and older are entitled to catch up contributions.

For illustrative purposes only. Employers are not required to offer or contribute to retirement plans.

The table also shows that an employer might match employee contributions. Matching contributions are not mandatory and not all companies offer them. When they do, an employer match could potentially boost retirement savings considerably.

In addition to your employer’s retirement plan (or in lieu of one if it isn’t offered), you can contribute to an Individual Retirement Account (IRA). Contributions may be tax deductible based on your income.

Limit Credit Card Use

Credit is an essential part of personal finance. Houses, cars and other necessities are often bought using debt. But going into debt to pay everyday living expenses can be dangerous – especially when credit cards are used.

Accumulating and carrying credit card balances can be a drag on retirement for two reasons.

- Credit card interest is typically higher than interest earned on savings

- Interest payments reduce investment opportunities

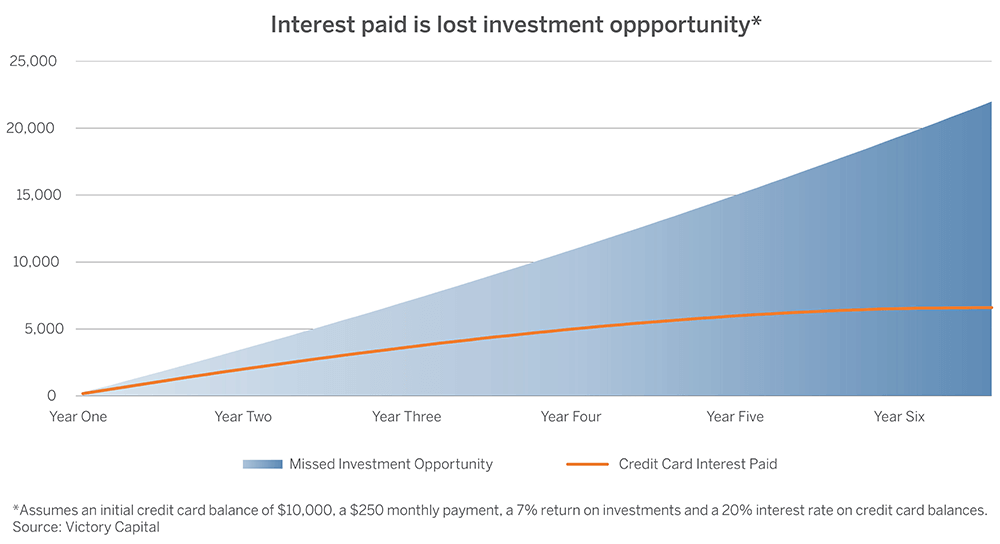

The chart below illustrates how carrying credit card balances negatively impacts personal finances.

In the hypothetical scenario highlighted above, it would take nearly seven years to repay the initial credit card balance. The total cost of financing $10,000 would amount to more than $6,500.

The monthly credit card payments required to repay that debt prevent funds from being invested. The missed opportunity amounts to nearly $22,000.

So, limiting credit card spending is a useful retirement planning technique.

Manage Social Security

Social Security should be considered as part of your retirement planning process. Benefits are based on wages while you are working.

The more you make, the more you contribute (up to a limit). Benefits are calculated using your highest earning years. Keeping track of this is important.

The Social Security website can help. It maintains a record of your contributions and calculates your estimated future benefits. Estimating your future benefits can be a valuable part of your retirement plan because they depend on timing.

If benefits are taken early, they will be reduced. Full benefits become available at the Social Security Administration’s “full retirement age”. If benefits are delayed, the amount increases.

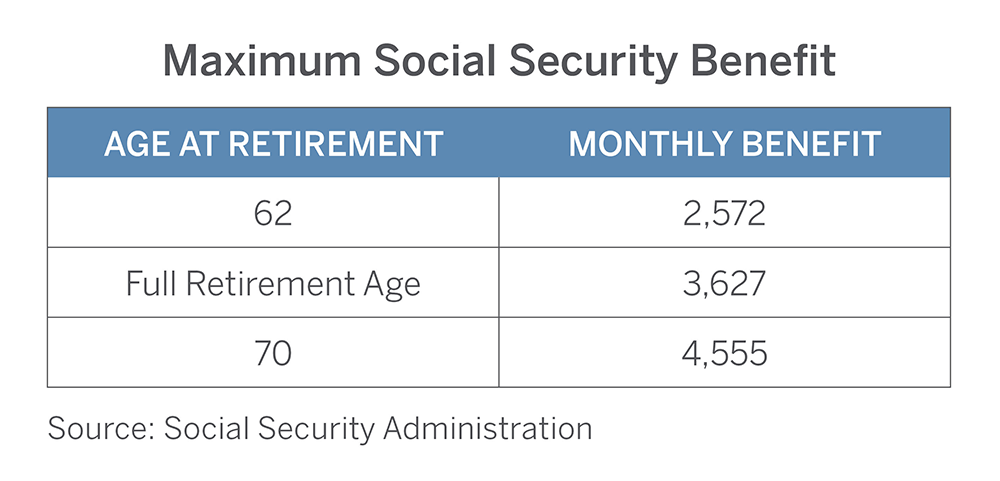

People can receive “early” benefits the year they reach age 62. If taken at age 62, benefits will be about a third of the full amount. The reduction is less severe for each month you wait to receive benefits. Your full benefit is available at full retirement age, between 65 and 67 based on the year you were born.

If you delay benefits beyond full retirement age, they increase slightly for each month they are postponed until you reach age 70.

Waiting until age 70 will add about a third to the full retirement benefit. The table below highlights the maximum benefit amounts for someone retiring in 2023.

Managing Social Security benefits during retirement means considering other sources of income – regardless of the age you start taking benefits. One goal might be to mitigate taxes.

Taking Social Security and working before full retirement age could subject benefits to both reductions and income tax. Delaying Social Security beyond full retirement age might increase your benefits, but your other sources of income could make a greater percentage of them subject to taxes.

Managing Social Security is also an important component of retirement planning because some sources of income – such as required minimum distributions – cannot be avoided.

For help putting all of these pieces together use our Retirement Planner Calculator to run various what-if scenarios.